Stability of industries main task this year

China's full-year GDP growth rate for this year is projected to be around 8.5 percent, affected by a low base in 2020, especially in the first quarter of last year. The statistical base effect may mislead investors and policymakers, and misguide macroeconomic policies. So we need to pay attention to the issue.

The largest uncertainty is about the COVID-19 pandemic, as whether the number of cases will rebound is unclear. If so, the economic downside pressure will resurge in the early months this year, reflected by constrained retail and traveling.

Other downside risks, domestically, may concentrate in the financial sector.

First, local government debt. Fiscal stimulus was strong, while in some regions the fiscal condition worsened, especially in the central and western regions and Northeast China.

Second, a risk factor could be small banks. Although small and micro enterprises have been supported strongly through bank lending, the potential default risk still exists.

From my perspective, there is no need to set a GDP growth target during the 14th Five-Year Plan period (2021-25). At the beginning of 2020, because of large uncertainties from the pandemic, we were unable, and it was unnecessary, to set the goal. And it was the right decision made by the annual Government Work Report to not set specific growth target.

Other than setting the GDP growth rate target, from this year, China may anchor employment stability and inflation control as the mandates of macro policies. The GDP projection could provide the basic reference to predict the government's fiscal revenue and expenditure in the budget. And investors can make decisions based on the GDP forecast. The GDP figure should not be used as a standard to evaluate the performance of local government officials.

If we continue to focus on the GDP growth rate, it may push the local governments to set high targets which will lift up the implicit debt risk, as borrowing is a simple method of stimulating investment to drive the growth.

Third, the base effect will be difficult to explain.

Taking stabilizing employment and controlling inflation as the main objectives of macro policies is a common practice in various countries under the market economy. Now, all developed countries and most middle-income countries have abandoned the GDP growth rate as a goal of macro adjustments.

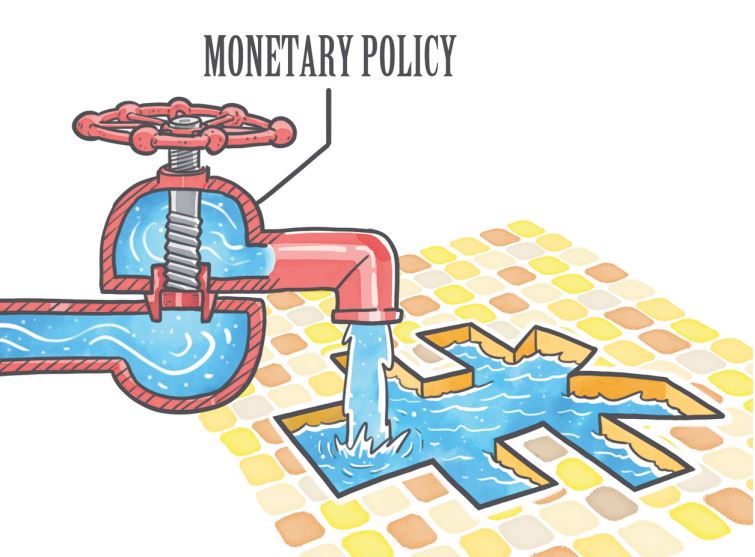

China's monetary policy should shift moderately. We are facing a dilemma. The fast rise of leverage ratio requires an adjustment of the monetary policy. In the first three quarters of 2020, China's macro leverage ratio increased by 25 percentage points, the largest rise since 2009, which may lead to potential risks in the future.

Bubbles are already in some areas. Last year, some major stock indexes were boosted remarkably at about 30 percent, and the bullish market in the economic slowdown was impossible to be unrelated to the monetary factor.

Meanwhile, home prices in Shanghai and Shenzhen, Guangdong province, are rising, which is related to the changes of liquidity and leverage ratio.

Whether this situation will intensify in the future will depend on whether the monetary policy should be moderately changed this year or not. If we don't shift the monetary policy, these issues will certainly continue.

On the other side, the monetary policy should not shift sharply. China's inflation is not at a high level right now. The CPI will look better this year because of the pork price's base effect last year.

The PPI will go up then, but not too much, which means the policy is unnecessary to turn too fast. At the same time, some local governments and commercial banks strongly demand to maintain the continuity of monetary policy, or require the transfer to be very slow. They think that if the transfer is too fast, it will lead to projects' shutdown, bad debts and other problems.

The Central Economic Work Conference held in December proposed that this year, China should ensure the growth rate of broad money supply, or M2, and total social financing, basically match the nominal GDP growth rate, and keep the macro leverage ratio basically stable. This means that the macro leverage ratio should not rise any further, but meanwhile, the policy should not make a sharp shift.

How does the growth rate of M2 match with the nominal GDP growth? In my opinion, it is relatively reasonable to maintain the M2 growth at about 9 percent.

The reasons are as follows:

First, the profitability of enterprises will be greatly improved this year. Many listed companies predict a profit growth of more than 20 percent this year. Owing to better profits, some enterprises are expected to reinvest their profits, so they can relatively ease their dependence on debt financing, and slightly lower the leverage ratio, thus, reducing the pressure on monetary expansion.

Second, monetary conditions should adapt to the adjustment of the broad fiscal deficit. Last year, China's broad fiscal deficit, which includes the general budgetary deficit, special anti-COVID-19 treasuries, and local government special bonds, was estimated to be 8.3 percent of GDP.

In the next two or three years, I think the proportion of broad fiscal deficit in GDP should gradually return to the level before the coronavirus crisis, such as down to 2.8 percent in 2019. With the decline of the broad fiscal deficit, the government will not issue so many bonds, which will then reduce the pressure on the expansion of monetary policy.

Third, the base effect. The base of China's real economy growth in the first half of 2020 was very low, which will make the year-on-year growth rate in the first quarter of this year very high. It is just the opposite for M2. Because the monetary expansion was very fast in the first half of 2020, the growth rate of M2 in the first half of this year may be relatively low.

I think we need to eliminate this illusion to see whether the money supply is adequate. An 8-9 percent growth is not low on a high base.

I suggest easing of some measures on forex outflows. The renminbi has appreciated nearly 10 percent since the middle of last year. If its value rises by more than 5 percent, there may be more pressure on exports.

Under the current situation, China should actively consider relaxing some specific measures on forex outflows, allowing some foreign capital to flow out of the country, which can reduce the pressure of renminbi appreciation. And we can take advantage of the opportunity of foreign exchange management system reforms to lay the foundation for renminbi internationalization in the next step.

Specific suggestions include simplifying the forex management methods for personal exchange, foreign direct investment by enterprises and foreign exchange retained by enterprises abroad.

Other measures include eliminating the quota limit of QDII (qualified domestic institutional investors), and speeding up the construction of channels for domestic investors to invest in overseas bond markets under the program of "Bond Connect". We can consider opening the southbound (to Hong Kong) trading to connect the international bond market.

The writer is a member of the monetary policy committee of the People's Bank of China, the central bank, and head of the Center for Finance and Development of Tsinghua University. The article is based on his speech at a seminar held by the China Wealth Management 50 Forum on Jan 14.

The views don't necessarily reflect those of China Daily.